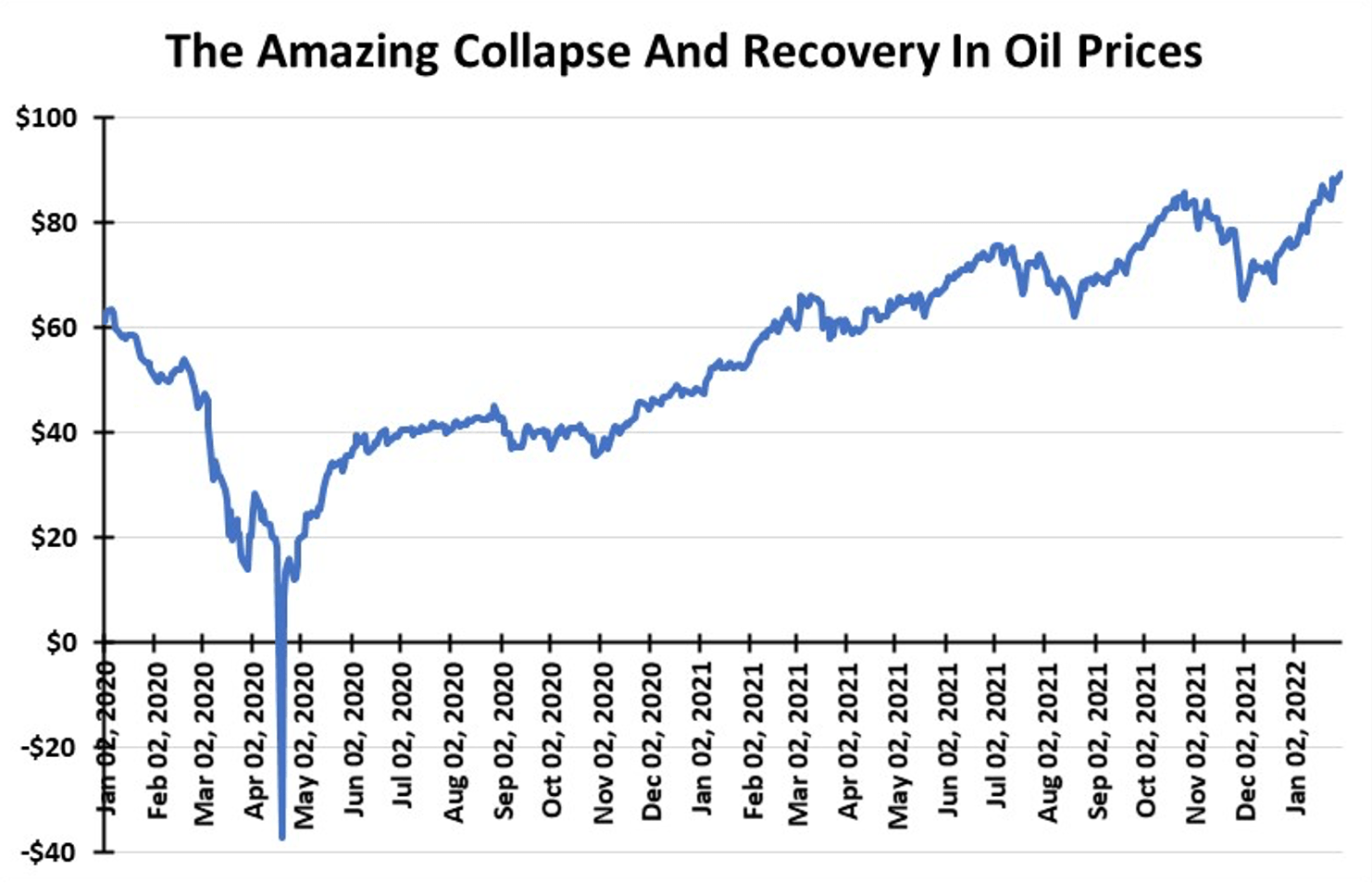

As the calendar flipped to February, the forces that sent WTI oil prices up 55 percent last year continued to drive them higher. As we complete the first week in February, WTI has advanced another 22.4 percent! Oil prices are above $90 per barrel, the highest price since September 2014 when oil prices were collapsing. This means consumers will face much higher gasoline pump prices—as high as $5 per gallon in California, and $4 in many other states—this spring. For residents in the Northeast, where heating oil is in strong demand, winter bills will be much higher than in previous winters.

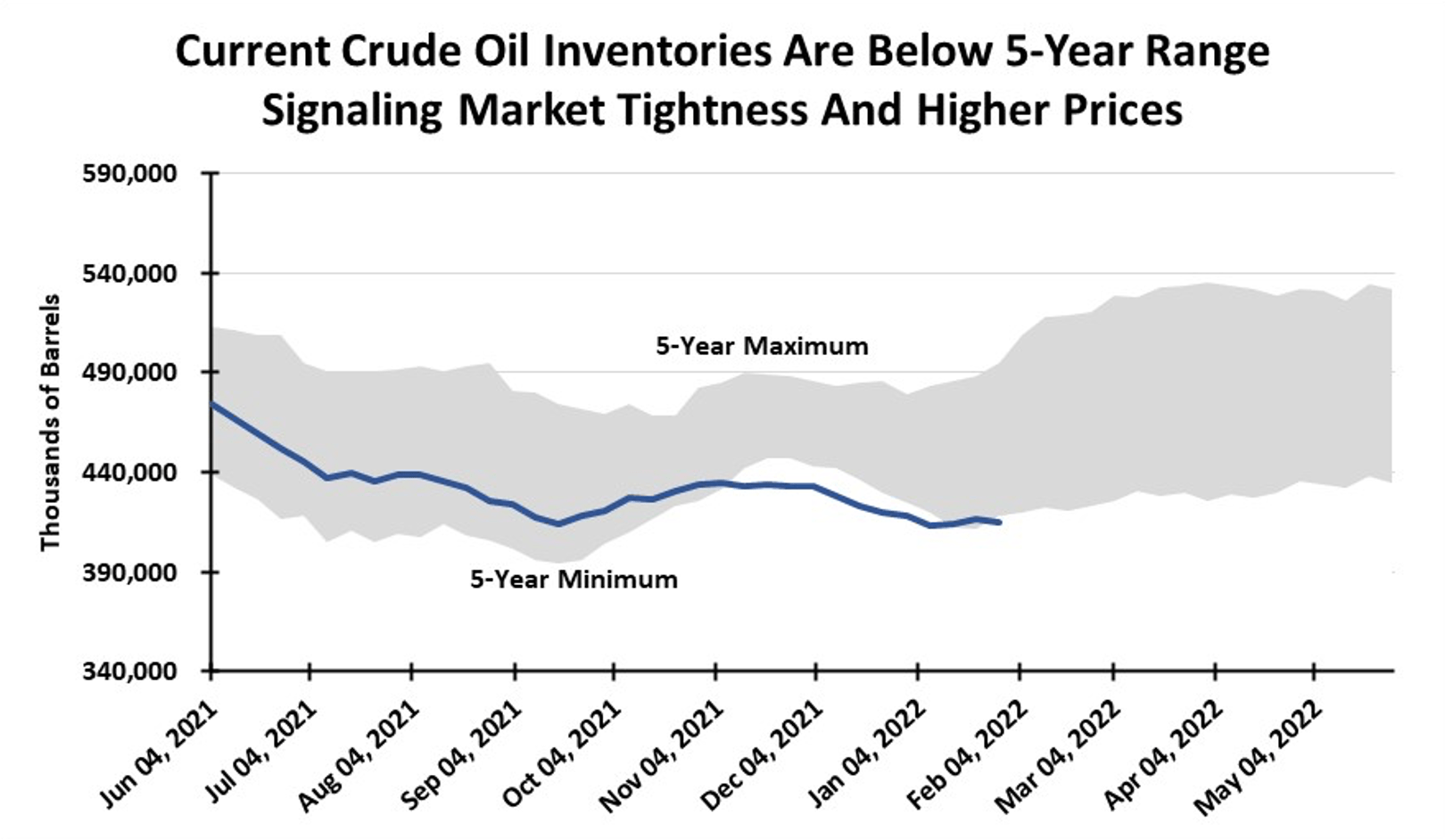

Is there any relief in sight? The short answer is No. The reason oil prices are this high, besides investors and speculators pushing futures prices up, is that the oil industry has experienced more than half a decade of underinvestment. Less money going into finding new oil reserves and boosting output means the power of natural oilfield production decline rates is limiting supply growth, thereby tightening the oil market and lifting prices. This is true not only in the United States, but in all oil producing countries around the world.

Is there any relief in sight? The short answer is No. The reason oil prices are this high, besides investors and speculators pushing futures prices up, is that the oil industry has experienced more than half a decade of underinvestment. Less money going into finding new oil reserves and boosting output means the power of natural oilfield production decline rates is limiting supply growth, thereby tightening the oil market and lifting prices. This is true not only in the United States, but in all oil producing countries around the world.

Last July, OPEC members, plus their Russian partner, pledged to gradually restore excess production mothballed following the pandemic related collapse in global oil demand in 2020. OPEC+ pledged to add 400,000 barrels per day of supply back to the market each month until the full surplus output is returned, which we be done later in 2022. The problem is that several OPEC members—Angola and Nigeria—have struggled to restore their offline production due to technical issues and aging deepwater fields. Even Russia has not fully met its increased production quota. Therefore, the market is growing skeptical of how much additional oil might be able to be pumped. That supply concern is contributing to higher global oil prices.

Oil prices seem to be locked into going only one way—up. The test of pricing’s strength will come in a couple of months when winter demand ends and before summer’s heat arrives. Sentiment is emerging that crude oil prices have risen too far and too fast and that the market is due for a correction. When it happens, the magnitude of the pullback may startle people. Could we see a price that starts with a six? That is not out of the question, depending on where prices sit when the correction begins.

Oil prices seem to be locked into going only one way—up. The test of pricing’s strength will come in a couple of months when winter demand ends and before summer’s heat arrives. Sentiment is emerging that crude oil prices have risen too far and too fast and that the market is due for a correction. When it happens, the magnitude of the pullback may startle people. Could we see a price that starts with a six? That is not out of the question, depending on where prices sit when the correction begins.

Would such a correction signify that the oil bull-market is ending? No. Bull markets, and commodity super cycles, are marked more by the duration of the above-trendline prices and not that they must continue rising. In other words, it is the amount of area under the price curve, and not the height of the curve that tells us about the likely longevity of this oil cycle. We think it has several years still to run.

Natural Gas:

Natural Gas:

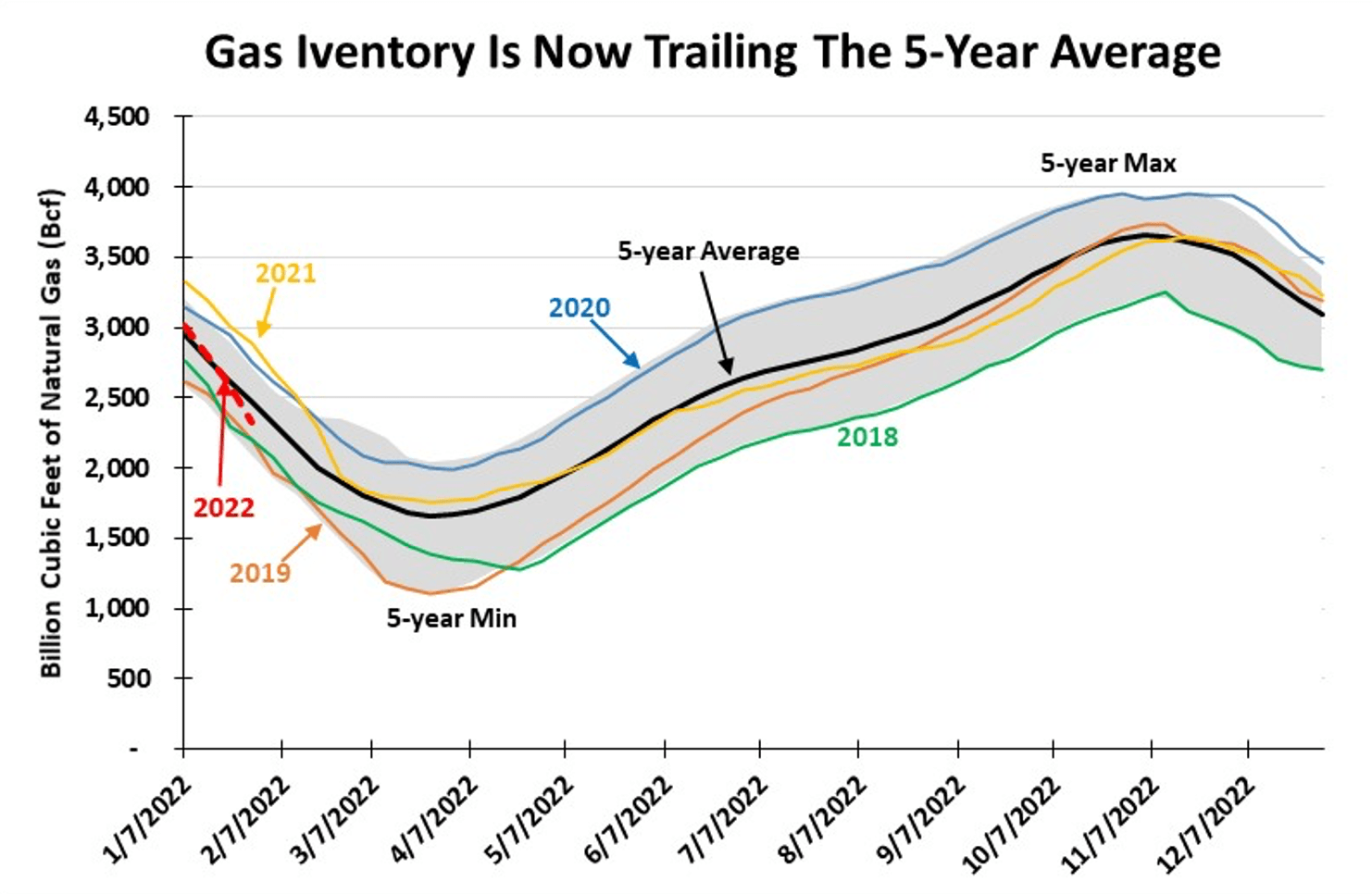

Winter is when natural gas prices often experience their greatest volatility due to shifting weather patterns. Storms and periods of bitter cold temperatures impact gas trader thoughts about their impact on gas demand, and in turn on how much supply will be withdrawn from storage. The more gas pulled from storage tanks and caverns means that much more demand will be experienced in the spring and summer when storage needs to be rebuilt to meet next year’s winter demand.

At the end of January, gas storage volumes fell by six percentage points below the 5-year average storage level, and more than twice that percentage shortfall from last year’s storage. Traders are viewing these shortfalls as signs the domestic gas market is adequately, but not overly supplied, meaning any increase in cold weather could generate greater supply concerns.

The latest estimates of daily gas production from IHS Markit show the volume to be about one billion cubic feet per day above the year-ago level. Marketed gas volumes have increased about 1.5 Bcf/d above last year, with liquefied natural gas shipments helping to lift those volumes.

So far this winter, due to a warmer-than-usual fall and early winter, domestic demand has been anemic with LNG deliveries taking up much of the slack. The United States federal government has been working to increase LNG shipments to Europe, given the continent’s worsening energy crisis, sky-high electricity and natural gas prices, and growing geopolitical pressures. Those shipments have knocked down spot natural gas and electric power prices in Europe by 30 percent, although they remain extremely elevated.

So far this winter, due to a warmer-than-usual fall and early winter, domestic demand has been anemic with LNG deliveries taking up much of the slack. The United States federal government has been working to increase LNG shipments to Europe, given the continent’s worsening energy crisis, sky-high electricity and natural gas prices, and growing geopolitical pressures. Those shipments have knocked down spot natural gas and electric power prices in Europe by 30 percent, although they remain extremely elevated.

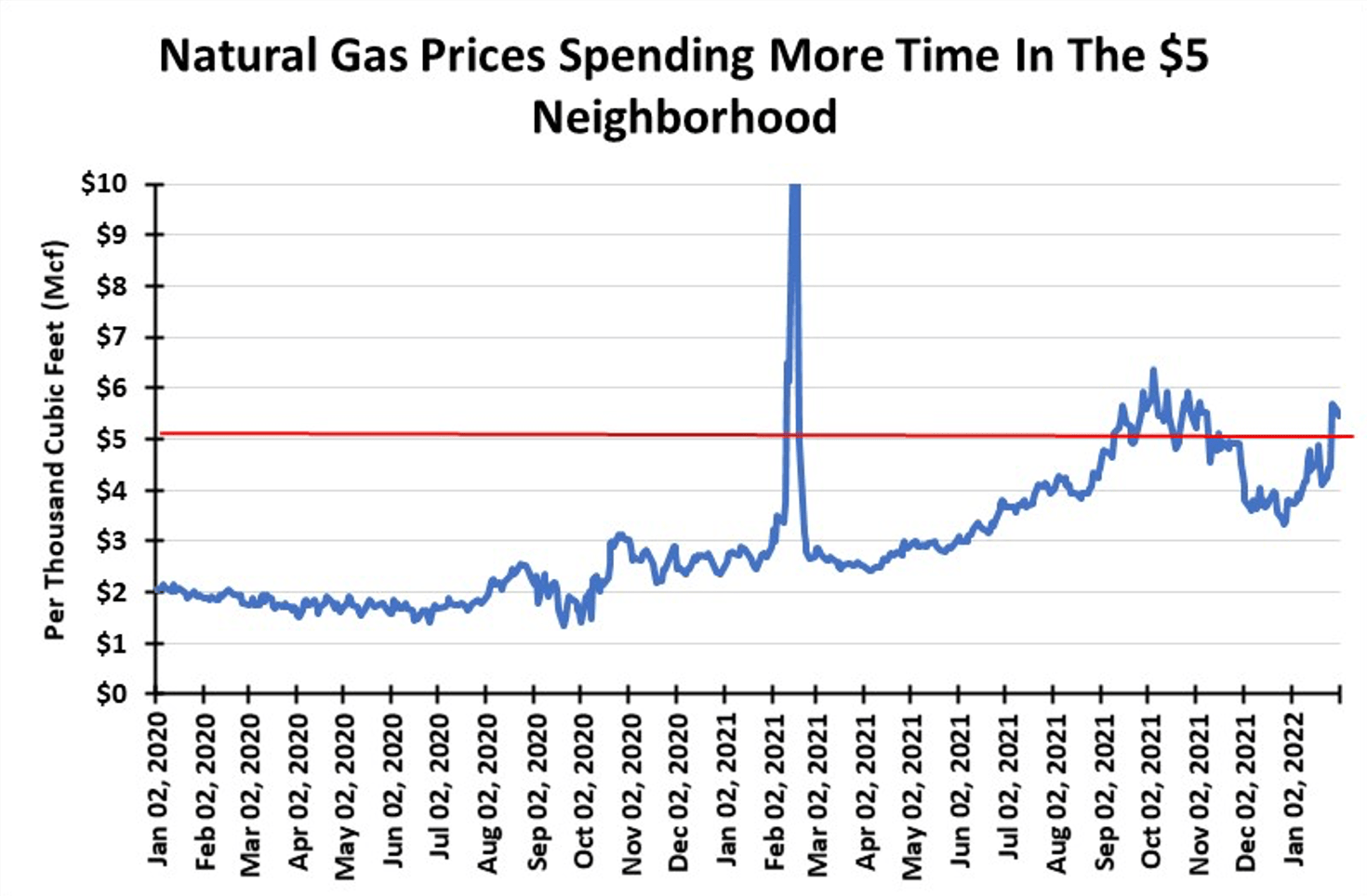

A bitter cold spell in the Northeast drove Boston spot natural gas prices to $30 per thousand cubic feet, nearly ten percent above comparable European gas prices. Those prices are nearly six-times higher than the Henry Hub spot gas price, ensuring attractive profit opportunities for natural gas producers, who are seen to be slowly increasing their drilling activity. In recent times, Henry Hub prices have been near or slightly above the $5/Mcf level, something not seen for many years.

Currently, natural gas traders believe Henry Hub spot prices are elevated due to the European situation. With winter’s end in sight, gas prices will be impacted by developments and sentiment regarding a possible military confrontation between Russia and Ukraine that could involve NATO and U.S. troops. Russia’s heavy hand in Europe’s natural gas business—supplying roughly 40 percent of the continent’s gas supply—ensures that these geopolitical tensions will continue to influence gas price thinking. The use of natural gas as a weapon in this confrontation could send European gas prices soaring, pulling along U.S. prices. Predicting the endgame for Ukraine’s political/military confrontation is impossible, thereby ensuring gas price volatility.

Currently, natural gas traders believe Henry Hub spot prices are elevated due to the European situation. With winter’s end in sight, gas prices will be impacted by developments and sentiment regarding a possible military confrontation between Russia and Ukraine that could involve NATO and U.S. troops. Russia’s heavy hand in Europe’s natural gas business—supplying roughly 40 percent of the continent’s gas supply—ensures that these geopolitical tensions will continue to influence gas price thinking. The use of natural gas as a weapon in this confrontation could send European gas prices soaring, pulling along U.S. prices. Predicting the endgame for Ukraine’s political/military confrontation is impossible, thereby ensuring gas price volatility.

By G. Allen Brooks, Expert Offshore Energy Analyst & ON&T Contributor

This story was featured in ON&T February 2022. Click here to access the digital issue.