Liquidity in oil trading has been reduced by regulators lifting cash margin requirements to 100-150 percent of the value of the trade to protect financial institutions. This has caused traders and hedge funds to exit the business, reducing liquidity, and contributing to increased price volatility.

Russia’s invasion of Ukraine tops the geopolitical problems list, as Vladimir Putin weaponized his country’s fossil fuels in prosecuting the war. Added to Russia/Ukraine are China/U.S. tensions over Taiwan, and the bungled U.S. oil policies impact relations with Saudi Arabia and OPEC+. The last two geopolitical issues were manufactured by the Biden administration’s energy and foreign policies.

Fearing a backlash in the upcoming midterm elections due to high gasoline prices, Biden seized on our Strategic Petroleum Reserve as a tool to reduce pump prices rather than maintain the supplies for emergencies. Attacking oil companies and hampering their operations has been a key aspect of the Biden administration’s Green Energy agenda and it has now led to a 25-year low in diesel fuel inventories, risking the backbone of the nation’s transportation sector.

Rather than helping Biden and his Democrat colleagues in the upcoming midterm elections, OPEC+ cut output by two million barrels-a-day. Since few OPEC+ members are producing at their quotas, oil supplies will only fall by 600 to 900 thousand-barrels-a-day. Thus, the global oil market will remain tight even with recessionary conditions emerging to we a kening consumption.

The big supply unknown this winter is the impact of the ban on Russian oil sales starting December 5. That ban will be followed by a Russian refined product ban commencing in February. These bans restrict not only the sale but also the shipping, financing, and insuring of Russian oil cargos. How much supply will cease flowing, and in which geographic markets is uncertain.

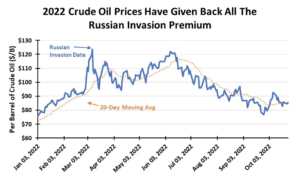

These bans will disrupt existing supply chains and raise concerns about the health of the global oil market. Fewer ships, less working capital available, and extremely high insurance costs will help drive up oil prices. If 500,000 to one million barrels a day of Russian oil and/or refined product cannot access the market, global oil prices could soar. Rising oil prices would also be helped as the headwinds from a strong U.S. dollar shifts to a weakening dollar. The latter condition is associated with historical $100+ oil price eras. About to happen again?

Help for higher oil prices may come from the reversal of the value of the U.S. dollar against other currencies. After years of strengthening, the dollar’s value is suddenly falling. That will make oil less expensive for international buyers, boosting demand. Here comes another driver for high oil prices, which is not yet receiving attention.

NATURAL GAS:

We are about to end the 2022 hurricane season with little impact on gas supplies or demand. Potential storms still lurk, but gas prices are awaiting winter weather and signals on LNG export demand.

Official U.S. government weather forecasts call for a moderate winter with few bouts of super-cold temperatures. In contrast, the Farmers’ Almanac expects a “Shake! Shiver! Shovel!” winter. We will experience a La Niña Triple-Dip (three consecutive years) for the first time this century and only the third time since weather records began in 1950. Such a weather phenomenon has been known to produce periods of severe cold and heavy snows, but also spans of more moderate winter weather.

The slowdown in U.S. LNG exports has enabled domestic storage volumes to grow faster in recent weeks, helping ease the shortfall that was helping elevate gas prices. For September and early October, gas storage injections were higher and the gap between current storage and 5-year average volumes closed. The latest week saw storage injections underperform leading to the storage gap widening.

Natural gas prices were above $9 per thousand cubic feet in both the spot and futures markets this summer. By the third week of October, prices were below $5, the lowest level in seven months. That price dip reflected storage injections growing just as media stories highlighted LNG carriers idling offshore Spain waiting to unload their cargos. With current European gas storage at nearly 100 percent full, Europe gas prices were dropping sharply. Those tankers are awaiting better gas prices. As the ships wait, Gulf Coast LNG exports stall.

Halloween traditionally marks the end of the high storage injection months and the beginning of winter demand, so prepare for further gas price volatility. Volatility will be driven by uncertainty over European LNG demand, which will now depend on heating and electricity demand. The economic contraction underway in Europe is sapping some gas demand as industrial companies cut back as sky-high energy prices destroy their profitability. Any early cold weather in the U.S. could easily spike gas prices as they are only restrained by expectations for soft LNG export demand. All gas markets are on a knife’s edge and poised to react to sudden weather and economic events. But winter will boost gas demand, so prices should strengthen in the weeks ahead.

This ENERGY MARKETWATCH was originally featured in ON&T’s November 2022 issue. Click here to read more.