The tightness developed from the speed of the global economic recovery following the COVID-19 shutdowns in 2020. Fear of the unknown from Russia’s invasion helped drive the WTI price to $124 and Brent to $133 per barrel. With Russia unable to roll over Ukraine, the global oil market began assessing reduced risk of supply disruptions, so prices eased.

Demand for most commodities—fuel and food in particular—is inelastic, meaning their demand is largely insensitive to changing prices. People need to drive; homes must be heated in the winter and cooled in the summer if people are to live comfortably; and food is necessary because people like to eat three meals a day. When prices for these commodities rise, people respond by limiting their use or substitute alternatives, but they do not stop doing these activities entirely. It would destroy lifestyles, something people will fight.

For crude oil, the petroleum industry’s challenge was dealing with a demand recovery faster than anticipated while the industry still struggled to manage the fallout from an extended period of low oil prices. It upended business operations leading to large job losses, compromised supply chains, and limited investment in new productive capacity. Such forces can be tolerated for short times, but not for five to seven years. Over such a long period, productive capacity is sapped, which must be replaced before supply can grow. In the U.S., domestic oil output was at 9.5 million barrels per day in December 2014 when the OPEC oil price war commenced. Two years later, U.S. production had fallen by 700,000 b/d. Better prices and the shale oil revolution’s success lifted output to 12.9 mmb/d in December 2019, but it fell by almost 2 mmb/d during the pandemic year of 2020. The most recent weekly government estimate shows domestic production of slightly over 12 mmb/d. The production surge came in response to the high oil prices we have lived with during the first half of 2022.

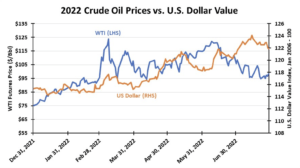

Oil prices have declined steadily since early June, falling 26 percent to $88 per barrel in early August. Helping drive the price down was a strong U.S. dollar, but that trend is beginning to reverse. Since the June price peak and despite periodic rallies, oil prices have consistently been below their 20-day moving average. Futures prices suggest that by August 2023, oil prices will be in the low $80s, or about where they were in January 2022. The current price decline comes with China’s economy still locked down and 1 mmb/d of oil released from our Strategic Petroleum Reserve adding to supply. Those conditions will change in the fall, and we still have the December 5 wildcard of Europe’s total ban of Russian oil purchases to consider. There is serious debate ongoing over whether the U.S. is in a recession, along with the rest of the world. If so, or a recession materializes later, oil demand will be hurt. With structural oil industry problems continuing, be prepared for volatile oil prices in response to events during the rest of 2022.

NATURAL GAS:

Natural gas prices have exploded to levels not seen since the 2000s. They are driven by a trifecta of forces: global demand for liquefied natural gas supplies, especially by Europe which is struggling to reduce its dependence on Russian gas supplies, is high; searing heat waves sweeping across the U.S. are boosting air conditioning demand; and gas production growth has been limited. These forces are shaping gas prices and given the demand for gas by economies around the world to meet power needs, the pressure is upwards. The U.S. LNG industry has been operating at maximum output in response to the extraordinarily high prices being paid for cargos in Europe that have exceeded what Asian buyers are willing to pay. That will not change anytime soon.

The accompanying chart of natural gas prices shows they peaked in late May, only to collapse shortly thereafter. That price drop resulted from a fire at Freeport LNG’s terminal on June 8 that forced it to shut down. The terminal represents 20 percent of U.S. LNG export volumes. With Freeport’s output lost until October at the earliest, gas traders expected the terminal’s supply would rebuild storage at a faster rate than predicted, therefore high prices were unnecessary to secure storage volumes. Summer gas prices reflect levels traders believe are necessary to induce producers to store gas for winter use.

Gas prices quickly rebounded following the shock of losing the Freeport terminal’s export volumes because the first heat wave in the western portion of the country emerged. Heat waves continued coming boosting gas demand for air conditioning. Temperatures remain elevated (it is summer) so gas consumption remains strong.

Regulators have indicated they will allow Freeport LNG to restart partial shipments in October, but that must still be considered tentative given the various safety tests yet to be completed. If the October date holds, the global gas market will breathe a sigh of relief, as the additional supply will be available by early winter.

High natural gas prices have enticed producers to add more drilling rigs, so we can expect increased supplies for the rest of the year. They will be needed because current gas storage volumes are lagging by 10 percent behind last year’s storage and 12 percent behind the 5-year average storage volume. Given the world’s need for more gas supply, global markets will have an outsized impact on U.S. gas markets and prices. Global and winter storage demands overwhelm any recessionary impact on gas consumption. Gas prices will remain elevated until the storage situation improves.

This story was originally featured in ON&T Magazine’s August 2022 issue. Click here to read more.