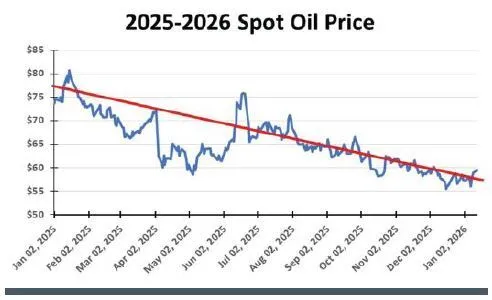

On the other hand, some forecasters are calling for oil prices to bottom around $55. They believe that the predictions of a massive supply glut misread the market and OPEC’s intentions, the major wildcard in the oil prediction business. As oil prices weakened in the final quarter of 2025, OPEC announced it would stop adding idled supply back into the market, as it had been doing monthly through much of the year. OPEC also called for an audit of member-nation production capacities. OPEC leadership wishes to make production quota decisions based on independently verified data, rather than relying on member-submitted numbers.

A significant consideration for the oil market is the health of the global economy. The latest data suggests that several troubled economies are improving, and some, like the United States, are posting growth rates significantly higher than anticipated. Germany just announced that its economy grew in 2025 after three years of contraction. Yes, the growth was helped by government spending, especially on military hardware, but the nation’s car industry, a significant sector, posted improving results during the latter portion of 2025.

The US economy shocked analysts with a 4.3 percent Gross Domestic Product growth rate in the third quarter, well above the forecast of 3.2 percent, and the fastest quarterly growth in two years. The third-quarter shocker followed the 3.8 percent increase of the second quarter. Expectations for a 2026 slowdown to only 2 percent will be re-evaluated as more year-end economic data is released and economists zero in on what the Federal Reserve will do with interest rates. Already, we have seen stronger homebuilding data from December, suggesting that the Fed rate cuts last fall have boosted one flagging economic sector.

The events in Venezuela in recent days and the political protests in Iran have lifted oil prices off their low $50s-a-barrel floor, as supply risks are beginning to be priced into the market. In recent days, oil futures prices climbed above $60, something not seen since mid-November.

Will leadership changes in Venezuela lead to a return of international oil companies and a sustained recovery in the nation’s oil output? Developments suggest yes, but history suggests being cautious about the optimistic prediction timeline.

The future of Iranian oil supplies, given the nation’s political unrest and sanctions against its sale, is a wildcard in near-term oil forecasts. Adding to this uncertainty is the state of the Russian economy, as a result of its ongoing war with Ukraine.

Given market dynamics, geopolitical risks, and strengthening economies, we may see oil prices trading in the $55–65 range for a while until greater clarity emerges about the outlooks of key suppliers and consumers.

NATURAL GAS

With oil’s dismal outlook, traders shifted their focus last year to the natural gas market. A driver of their increased interest was surging electricity demand, fueled by massive investments by technology companies in new data centers to support the uptake of Artificial Intelligence algorithms. The electricity industry, which had experienced only 1 percent annual demand growth for decades, is suddenly experiencing 5–7 percent annual growth.

To appreciate how these forecasts are shaking up the power industry, we should note that such rapid growth in electricity demand has not been seen since the 1950s and 1960s. The 1970s and 1980s saw electricity demand grow at 3–4 percent annually, and in the 1990s it fell to closer to 2 percent. Since 2000, annual electricity growth has been 1 percent or less annually, with extreme volatility around COVID.

As electricity demand is exploding, it is running into the climate change dynamic that has been the overarching driver for electric industry supply planning. The political embrace of climate change forced utilities to accept building a grid based on renewable energy. Wind and solar have been promoted as cheap, but that claim is based on calculations that ignore the physical realities of the grid. As renewable energy’s share of total power grew, its rate of penetration was helped by the retirement of coal-fired generating plants.

The explosion in electricity demand has placed the grid’s performance at the center of the debate about power supplies. Data centers require power 24/7, which means they require dispatchable power sources such as nuclear and fossil-fuel-generated electricity, rather than intermittent renewable energy. Lower emissions from natural gas power plants have made them a desired fuel source for electricity generation.

As electricity needs increase, natural gas consumption is growing. Similarly, power and clean energy demand internationally are boosting the liquefied natural gas business.

Concern is growing over whether the US has the gas supplies to feed two hungry sectors. Recently, a proposed LNG terminal was canceled because rising construction costs squeezed the developers, while buyers were reluctant to sign long-term contracts to support the debt needed for construction.

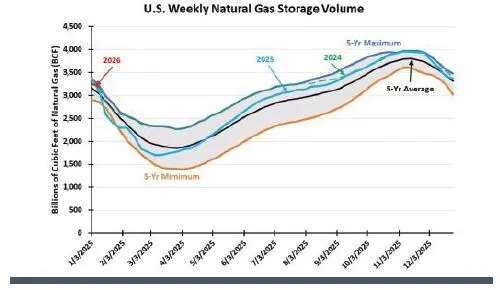

While natural gas consumption markets wrestle with prices and supply, near-term gas prices are bouncing in tune with weather conditions. This is not a surprise, as price volatility is experienced every winter. The first two weeks of January saw one very cold and one considerably warmer. Unsurprisingly, gas prices jumped up and then fell.

The underlying long-term demand trend for natural gas is upward and will support rising average annual gas prices after years of sub-optimal pricing. Along the way, traders will have opportunities to profit from the weather.

SPOT OIL PRICES CURRENTLY REFLECTING GEOPOLITICAL TENSIONS

WEATHER HAS GAS PRICES ON A ROLLER COASTER; NOT SUPPLY ISSUES

This feature appeared in ON&T Magazine’s 2026 February Edition, Exploring the Deep, to read more access the magazine here.