Traders understand that any military conflict would likely disrupt the oil flow through the Strait of Hormuz. Roughly 20 percent of the world’s oil and LNG travels through the strait. Negotiations between the US and Iran over its nuclear enrichment policy are ongoing, but neither side is compromising.

A fallout from the West’s efforts to end the Ukraine-Russia war is increased sanctions on Russia’s oil industry. Sanctioned oil tankers are being targeted for arrest to limit Russia’s oil exports. Many of them are reflagging under the Russian flag, increasing the risk of military conflict and further boosting the oil price risk premium.

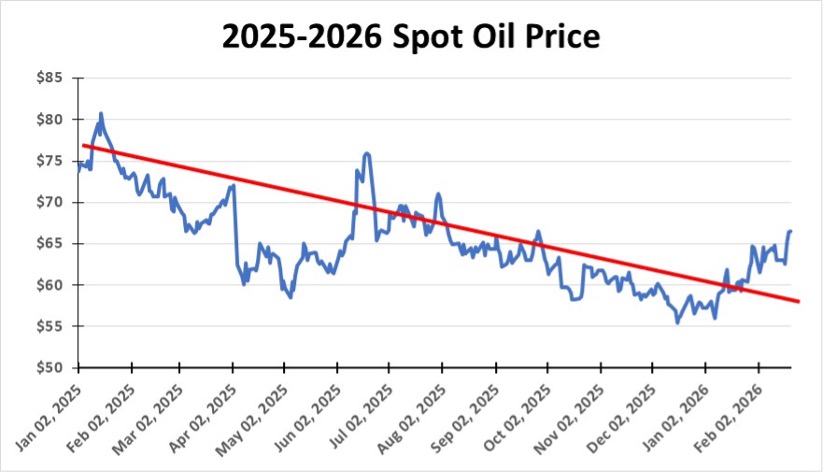

The fundamental industry outlook hasn’t changed. The International Energy Agency (IEA) sees weak oil demand and strong oil production creating a huge glut. OPEC producers are still returning idled output to the market to capitalize on higher oil prices. The IEA projects Brent oil prices will drop from an average of $69 a barrel last year to $58 this year and $53 next year. This price profile encourages producers to maximize current production.

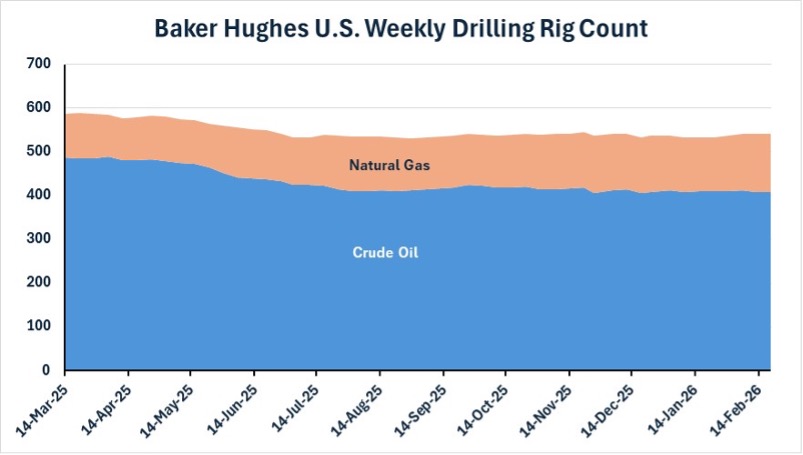

The US Energy Information Administration continues to forecast high domestic oil production, despite lower drilling activity. Compared to a year ago, the oil rig count in mid-February is down 16 percent, a loss of 79 rigs. The count fell to 406 in mid-December and has remained essentially flat since then. The decline in drilling activity will affect future shale oil output, as wells struggle to sustain production. The supply glut could shrink more quickly than anticipated.

The exact opposite has occurred for natural gas drilling, as its rig count has increased by 33 percent over the past year. More gas drilling is happening because gas prices are up, as is consumption.

Oil companies are returning to their core business as they scale back or eliminate their green energy ventures due to profitability concerns. They are also being encouraged by the IEA to step up exploration, which is forecasting rising oil use through 2050. Moreover, the IEA is telling the industry that its lack of investment in recent years has increased the risk of higher oil prices. This isa reversal by the IEA, which US Energy Secretary Chris Wright has chastised for abandoning its mission to produce realistic rather than aspirational forecasts.

Volatility will continue to swirl around oil prices, given the fuel’s crucial role in global economic activity. Geopolitical tensions impacting oil prices have now returned after years of little concern. Stronger economic growth, which looks more likely, could materially alter the oil glut and low oil price narrative. Time will tell.

NATURAL GAS

Last month, our column preceded the arrival of Winter Storm Fern, which swept across the Lower 48, delivering bitter cold and substantial ice and snow. Electricity grids in most regions were seriously challenged; fortunately, there were no major blackouts.

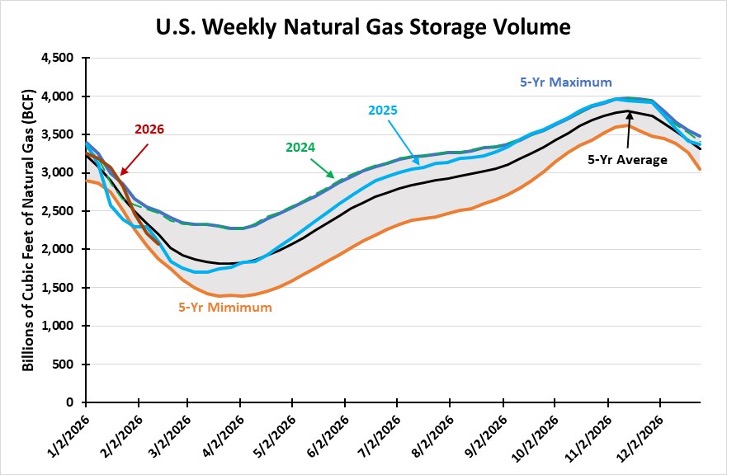

Fern demonstrated the critical role that natural gas plays in keeping the lights and heat on. Gas consumption during the storm week resulted in the largest drawdown of gas storage in the EIA’s history of record-keeping. The nation’s gas utilities withdrew 360 billion cubic feet, 89 percent higher than the five-year average for that week. Illinois utility Nicor described how it used gas storage to meet 43 percent of customer demand during the storm.

While the public focused on blackouts, it was shocked by how high spot natural gas prices soared. When cold weather arrived the week before Fern, gas prices jumped to over $10 per thousand cubic feet, only to soar to nearly $14 during the storm. Immediately after Fern, with storage only 1.1 percent below the 5-year average, gas prices dropped by more than half before returning to the $3/Bcf range the following week. Although gas storage is now nearly 6 percent below the 5-year average, gas prices are benign as the market anticipates spring, despite Punxsutawney Phil seeing his shadow and calling for 6 more weeks of winter.

Barring another polar vortex, the US will end the winter withdrawal season with typical gas volumes in storage, which is not positive for gas prices. However, LNG volumes continue to rise, which helps support prices. The debate over whether we can consume greater volumes of gas for generating electricity in the new data centers being built, while also exporting more LNG and not sending gas prices soaring, is ongoing.

The latest production forecast from the EIA offers comfort about gas prices. It sees production rising by 2 percent this year, and about 1.5 percent in 2027. Will that be sufficient to keep gas prices at $3/Mcf. People and the market should prepare for gas prices around $4/Mcf, which would be higher than experienced for most of the last decade, as LNG export volumes grow. What we do not want or expect to see are gas prices below $2/Mcf or above $8, outside of weather events.

While weather demand, LNG export volumes, and domestic production will be discussed, the greatest debate will be the need for gas supply for data centers. They have displaced climate change from the debate over natural gas’s role in the electricity industry.Natural gas is becoming more than a bridge fuel to the future.

GEOPOLITICAL TENSIONS RAISE OIL PRICES BUT HAVE NO IMPACT ON DRILLING

THE GAS INDUSTRY WEATHERED FERN, UNDERSCORING THE FUEL’S CRITICAL ROLE

This feature appeared in ON&T Magazine’s 2026 March Edition, Unmanned Naval Defense, to read more access the magazine here.