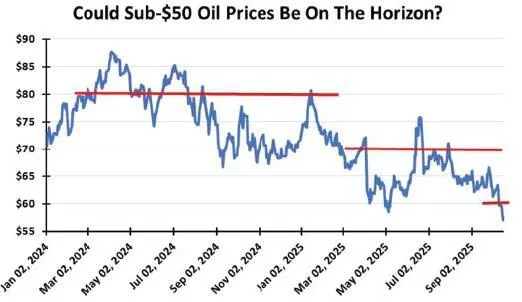

Oil prices have fallen below $60 a barrel. The Energy Information Administration (EIA), as well as numerous forecasters, are predicting prices will fall below $50 a barrel soon and continue through 2026. Such a low price will alter producer and consumer actions. The former stop drilling and the latter buy more.

For the last three weeks, the US has experienced higher weekly oil storage builds than predicted by analysts. The storage surge is being treated as a sign of major market problems, although the current inventory level is barely above the average of the last five years.

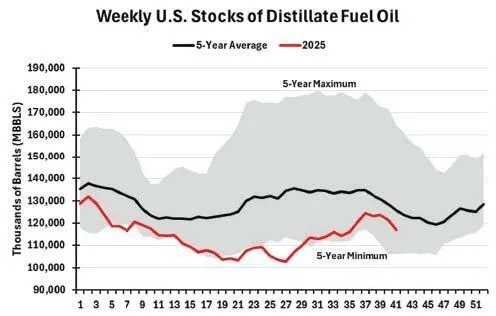

When we examine gasoline and distillate storage levels, the former is in line with the five-year average, while the latter remains below the average. Distillate inventories remain a concern, as this fuel is the source of home heating oil for portions of the United States during the winter, and it is the fuel that powers our rail and trucking activity, critical for the functioning of our economy. The current level of distillate storage has recovered from its extremely low levels earlier this year. Still, in the last few weeks, storage levels have fallen faster than the five-year history would suggest is normal. A problem on the horizon?

With the tariff wars heating up and peace breaking out in the Middle East and Europe, the concern is that the global economy will slow while more oil supplies land in the market. The International Energy Agency (IEA) has cut its global oil demand growth estimates to 700,000 barrels per day for both 2025 and 2026. That is a rate well below the growth forecasted by OPEC and our historical growth rate.

The IEA has also increased its estimate of global oil supply growth for both years. In the US, producers are beginning to stop drilling, but output remains at record highs. It will take time for production to start falling, but given the nature of shale oil output, the drop could be sharp without sustained drilling.

OPEC has recently hired consultants to assess the productive capacity of its member countries. Officials no longer want to rely on the self-assessments of output capacity, as they may be influenced by political considerations, rather than physical realities. Could OPEC be out of additional supply capacity?

Other geopolitical wildcards could alter the global oil market. Will global peace initiatives bring more oil to market? Or might tighter Russian sanctions limit supply? We are told that India will no longer purchase Russian crude. If it is true, where will that oil go, and at how low a price? Do not unquestioningly accept the consensus view.

NATURAL GAS

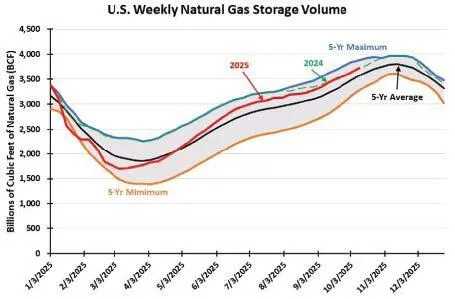

Natural gas volumes currently in storage are about equal to last year’s. Storage volumes are about four percent above the five-year average. The injection rates of the previous three weeks are equal to those of the same weeks last year. What was different was that August’s weekly injections averaged about double the injections during August 2024. We attribute the differential to this August being cooler than August 2024. Although August is a summer month, there are regional differences in average temperatures, which impact air conditioning use and, therefore, the volumes of natural gas burned to generate electricity.

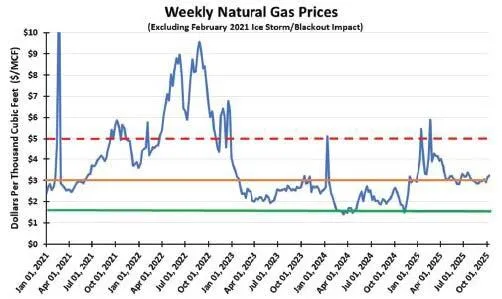

As we head into fall and winter, gas demand for air conditioning will decrease as temperatures and humidity drop. Until cold weather arrives, driving heating demand, natural gas markets will be impacted more by exports, primarily LNG, and industrial consumption. The latter is facing weaker consumption as the US economy appears to be slowing. These dynamics have kept gas prices essentially flat since April.

The Energy Information Administration, in its most recent natural gas weekly report, noted that 32 LNG cargoes departed US terminals. We do not believe this is an extraordinary number of cargoes, but rather reflects the significant role that cheap American natural gas plays in the world’s energy markets. This role has become a focal point of multiple countries’ energy policies.

The most significant policy battle is between Qatar and the European Union over its Corporate Sustainability Due Diligence Directive. Qatar supplies 12 percent to 14 percent of Europe’s LNG since the start of the Russia/Ukraine war. However, the EU’s directive, which requires larger companies operating in the EU to find and fix human rights and environmental issues in their supply chains or face financial penalties, may prevent QatarEnergy from conducting business with the EU. The financial penalties for failing to have climate change transition plans aligned with the Paris Agreement goal of preventing global warming from exceeding 1.5 degrees Celsius are fines up to five percent of total global revenues. That is totally unacceptable to Qatar.

Should the EU not relent, it could face a significant overhaul of its LNG supply chain, in addition to its decision to stop allowing the burning of Russian LNG. This political battle comes as concerns about a future global glut of LNG arise. Those concerns are coming from the aggressive expansion plans of US LNG operators, even though exporters do not build terminals on speculation, only after they have secured long-term off-take contracts. This glut fear may be like other times—overblown, as concerns about large supply increments always seem to follow announcements of new export terminals.

Natural gas and LNG remain a critical bridging fuel for reducing emissions. The example of the US should not be lost on other countries, as we have sharply reduced our emissions since 1990 by substituting natural gas for burning coal to generate electricity.

FEAR OF A GLUT IS DRIVING OIL PRICE FORECASTS

GAS STORAGE IS ADEQUATE HEADING INTO WINTER

This feature appeared in ON&T Magazine’s 2025 November Edition, Remote Operations & Force Multiplication, to read more access the magazine here.