Recently, Russia added to the market’s woes by instituting an embargo on one million barrels a day of diesel fuel and 500,000 barrels a day of gasoline exports. Ostensibly, Russia’s move was to help its domestic market by ensuring greater supplies to keep prices from flying up as crude oil prices soared.

Diesel is the workhorse of the global transportation industry powering heavy-duty trucks, trains, and maritime vessels. Everything we make, grow, process, and consume is touched by trucks, trains, and boats. Already, long-haul trucks moving food products to grocery stores across the nation are adding fuel surcharges to their bills to offset the high cost of diesel. We will experience greater inflation and it will be across the board.

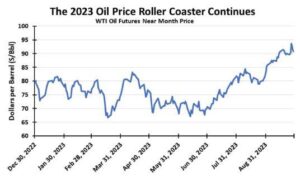

The unified strategy of OPEC+ to constrain global oil supplies has resulted in shrinking crude oil and refined product inventories. Lower inventories are helped by Western oil company’s strict adherence to capital discipline. As oil prices have climbed, the US drilling rig count has fallen. Despite being pressured to step up drilling to capitalize on high oil prices, producers understand that one twist of the valve in Saudi Arabia and oil prices could drop, turning profitable plans into losing projects.

Saudi Arabia has concentrated its production cuts on the oil that makes the most diesel fuel. Thus, they are ensuring distillate stocks will struggle to grow heading into winter when cold weather pushes up demand. Over the past two years, the refining industry has shut down or transitioned to producing sustainable aviation fuel the industry’s small, unprofitable refineries. New refineries are due to start up at the end of the year and during 2024, which will boost crude oil demand next year. Expanded refinery capacity will enable petroleum product supply to grow next year, which should ease product prices but support high crude oil prices. The direction of oil prices—above $100 a barrel, flat around $90, or falling into the $70s and $80s—will depend on economic activity and winter weather. Remember, we remain a geopolitical event, supply accident, or demand shock away from a volatile move for oil prices.

NATURAL GAS

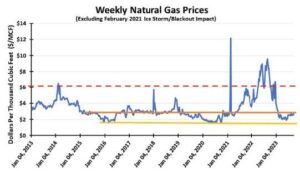

Natural gas prices continue to strengthen as hot weather has just begun to moderate, while liquefied natural gas (LNG) exports continue to climb. We will be reaching a point soon when the air conditioning load ends, yet heating demand has not materialized. Demand slumps for a brief period. That condition could be extended if we experience another warm winter. Some weather forecasts suggest that the arrival of El Niño conditions may cause a warmer winter. However, many weather forecasts are calling for a colder and wetter winter. We have already seen early snow and cold weather. Betting with or against Mother Nature is dangerous.

LNG is the key driver for natural gas demand and price. European gas storage is nearly full, well ahead of the start of winter. As a result, European gas prices have dropped. LNG exporters will not be making the outsized profits they did last year when they were buying $2 gas and selling it for $12–$14 a thousand cubic feet to bail out Europe from its energy crisis created by the Russia/Ukraine war. Currently, Dutch TTF gas futures prices are a fraction of what they averaged during 2022, but when winter arrives, the continent’s storage is insufficient to meet the entirety of winter gas needs. Therefore, the recently constructed LNG import terminals will become busier, and one suspects the gas crossing those terminals will be higher priced than current TTF prices.

Natural gas production continues to climb as many Permian Basin oil wells become gassier. That naturally occurs when an oil well’s output declines. Then high-pressure gas dissolved in the reservoir’s oil is released by the lower pressure. The surge in Permian gas output is forcing the industry to build new pipelines to move produced gas either to the Gulf Coast for LNG exports or to Mexico. Additionally, more gas processing plants are being built to extract the natural gas liquids from the gas output streams to meet growing petrochemical and other uses.

While the Energy Information Administration (EIA) has trimmed its natural gas growth projection forecast for 2023 from 4.9 percent to 4.7 percent. It has doubled its 2024 growth estimate from 1.1 percent to 2.2 percent, pushing estimated daily output to a record 105 million cubic feet per day. There is little concern within the producer industry that it can meet the nation’s growing gas needs.

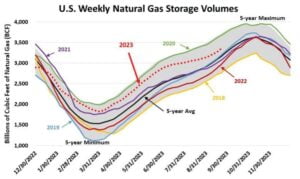

Absent any surprise event, natural gas prices are likely rangebound until deeper into winter when traders begin focusing on what it will take to rebuild storage volumes for the 2024–2025 winter. So far, gas storage volumes are moving closer to the middle of the historical range, which has been accompanied by higher gas prices to entice more storage volumes. Expect this to be the norm for the next few weeks or possibly months before prices strengthen in early 2024.

This story was originally featured in ON&T Magazine’s Oct/Nov 2023 issue. Click here to read more.