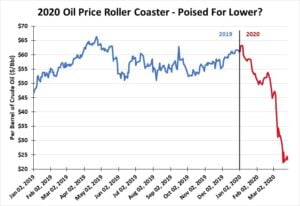

The recommended output cut was anticipated being embraced at the early March OPEC-plus meetings and would forestall an oil price collapse. Our assumptions proved wrong and oil prices fell 53 percent in the 10 trading days following the failed OPECplus meetings!

While a disagreement over the magnitude of the OPEC-plus output cut increase was a distinct possibility, no one envisioned the disagreement leading to an all-out oil war between Russia and Saudi Arabia, two of the world’s largest oil producers. Saudi Arabia aggressively moved to cut export prices – especially for its Asian customers who Russia was targeting – and boost production to record levels. This appeared to be a “scorched earth” strategy, designed to teach everyone, especially Russia, to not “mess” with Saudi Arabia.

On April 1st, Russia will restore its 280,000 barrels a day output cut, but whether it can add an additional 500,000 b/d, as announced, remains questionable due to logistical challenges. In the meantime, Saudi Arabia instructed Aramco to ramp up production capacity to 13 million barrels a day, and immediately boost shipments by 2.5 mmb/d to 12.4 mmb/d. This incremental supply, combined with continued growth in U.S. shale oil output, guarantees the world will be over-supplied with oil at a time demand is collapsing, as the world deals with the economic impact of Covid-19.

Estimates call for oil demand to drop by 10-14 mmb/d in April, ensuring storage tanks around the world will be overflowing. Even with adding tankers, such as Saudi Arabia’s recent contracting of 31 VLCCs, storage will be overwhelmed, pushing oil prices lower. With demand down and growing numbers of mandatory “shelter-in-place” orders shutting down not only cities but even countries such as Italy, Spain and India, refiners will take less oil despite sharply lower prices. The industry’s low-oil price playbook, which calls for ramping up refining as consumers respond to lower pump prices by increasing fuel consumption, will not work this time.

The combination of a demand shock from the virus and a supply shock from an oil-war presents a unique challenge for oil companies. Can the oil-warring parties reach an agreement to cut output? Not likely, at least anytime soon. Will we see a peaking in the virus spread, and then be able to predict when economies will restart? Possibly, but the timing is uncertain. Therefore, market conditions will weigh on oil prices. They likely go lower before rallying. Don’t expect a meaningful oil price recovery, however, until future supply/demand dynamics become clearer.

Natural Gas:

The one fuel seemingly benefiting from the market’s response to Covid19 virus and the outbreak of an oil war is natural gas. One wonders why? Especially when we focus on the calendar’s transition from late winter into early spring. It means cold weather becomes less of a gas demand driver, although often there is one last winter blast before the trees and flowers fully bloom.

With oil demand collapsing and prices in freefall, U.S. shale producers are slashing capital spending. Drilling activity is dropping and high-cost shale wells are being postponed. Fewer new wells plus rapid declines in oil shale well output means less associated natural gas will soon be flowing. An offset is that Permian Basin shale wells see more gas flowing as oil output declines. Overall, though, natural gas output will slow and eventually decline.

In the near-term, with gas supply growth slowing, natural gas prices will depend increasingly on demand factors – principally non-weather ones. That means natural gas for powering electricity generators, as well as for export either via pipelines to Mexico or as LNG to world markets. Low prices are boosting the global competitive position for U.S. natural gas.

Gas consumption for power generation was substantially above last year through the middle of March, and projections call for it to remain higher through the balance of the month. The reason for the elevated level is the increased shutdowns of nuclear power plants for maintenance. So far this year, nuclear plant shutdowns have been above the 5-year average and the shutdowns of last year. Natural gas generated power offsets that electricity loss.

An important driver for gas demand is coming from the LNG business, as volumes shipped in March will substantially exceed those moved last year. That largely reflects the additional LNG export capacity that began operating during the past 12 months. Shipping data shows 14 LNG cargoes will move from Coast export terminals during March. That good news, however, is offset by the announcement of two cargoes from Chenier’s Sabine Pass terminal being rejected by buyers. Cheniere’s high financial leverage, the inability recently to secure a long-term LNG deal with India, and the current market turmoil has forced the company to lay off a substantial number of employees and reduce executive compensation. Is bankruptcy in its future?

The last time natural gas prices traded below $2 per thousand cubic feet was in 2016, when oil prices were also diving. Market conditions eventually pushed the price back above $3.50. Traders believe the current oil market debacle will restrict gas supply growth, and as demand picks up, gas prices will rise. We could be surprised how far they climb. If it happens, producers will smile, but not consumers.

This story was originally featured in ON&T Magazine’s April 2020 issue. Click here to read more.