Every day, hundreds of ships pass through the Strait of Hormuz, entering or exiting the Persian Gulf, home to 20 percent of the world’s oil moved by sea, and an equal share of the world’s liquefied natural gas output. When the war commenced, this energy flow ceased as insurers stopped providing coverage for vessels that risked attack by Iran while transiting the Strait.

Crude oil prices soared due to the world’s largest oil disruption in history. Asian countries were the quickest to react, understanding that 90 percent of some countries’ oil and gas supplies were suspended. Countries reacted by restricting the export of refined petroleum products, opting to save it for domestic use. Various countries urged changes in work schedules and transportation to reduce oil consumption. Many governments urged switching home cooking fuels, and reducing the use of air conditioning.

Current oil prices are around $100 per barrel. Surprisingly, they didn’t reach as high as predicted in the early days of the Strait closure. The reason is that Saudi Arabia and the UAE have been able to export nearly 9 million barrels per day, reducing the global shortage by nearly half. There have also been the tankers that Iran allowed to leave, because they were carrying Iranian oil. The world is also drawing down global oil storage to offset the lost productive output.

In response, the US instituted a blockade, which cuts off Iran’s oil income. This is a problem for the government, as its economy was already reeling from inflation and its inability to provide sufficient goods for its citizens. Public protests have only been tempered by the government’s willingness to execute youthful protestors.

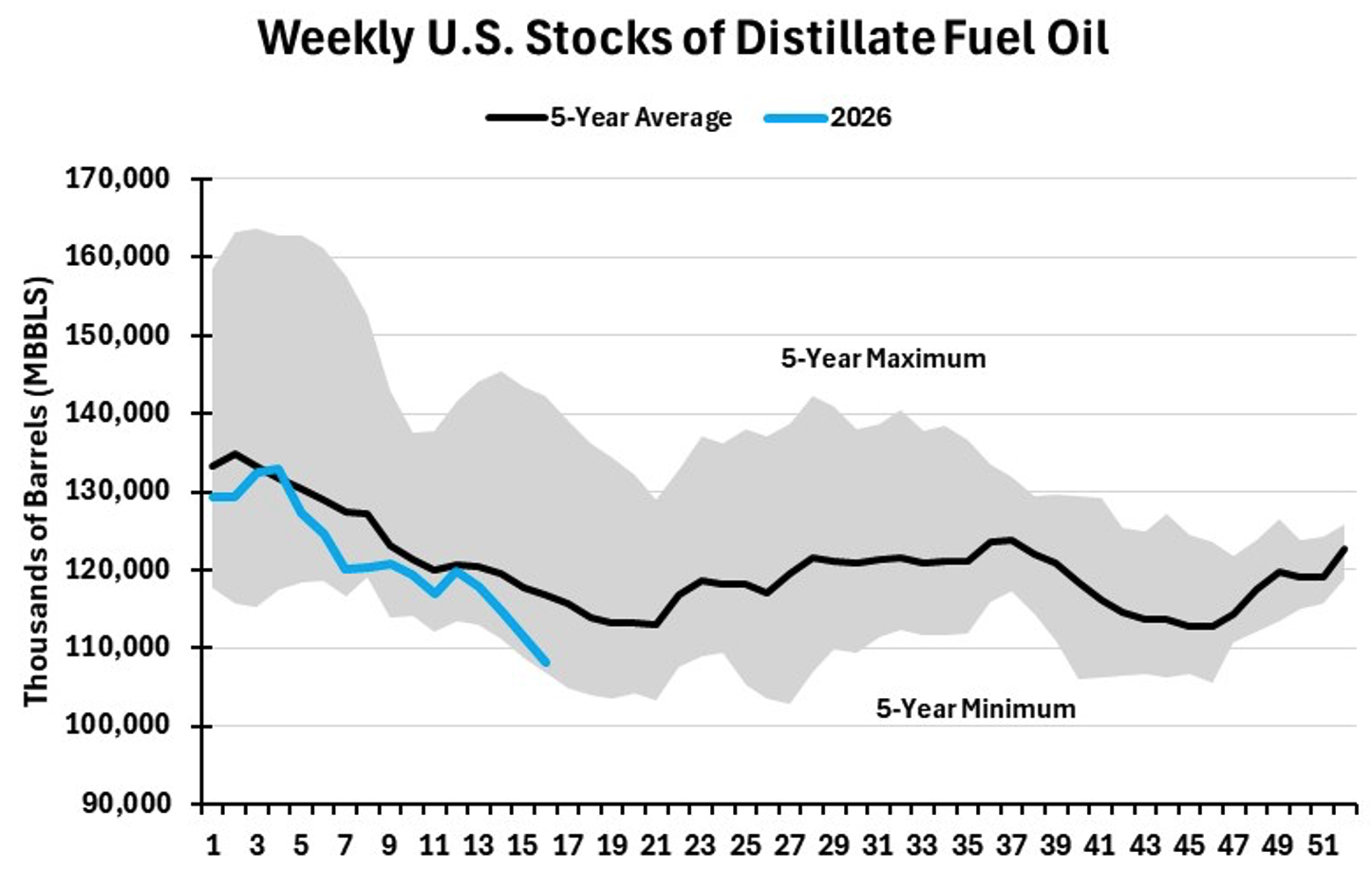

The world is learning that oil is the lifeblood of the global economy. Without oil, the quality of life is diminished. Could the US face a distillate shortage that impacts its domestic transportation?

Adapting to shortages is the greatest challenge governments must address. Each nation will need to assess its natural resources and internal capabilities; some will be better positioned than others. Will these changes become permanent, impacting future oil markets?

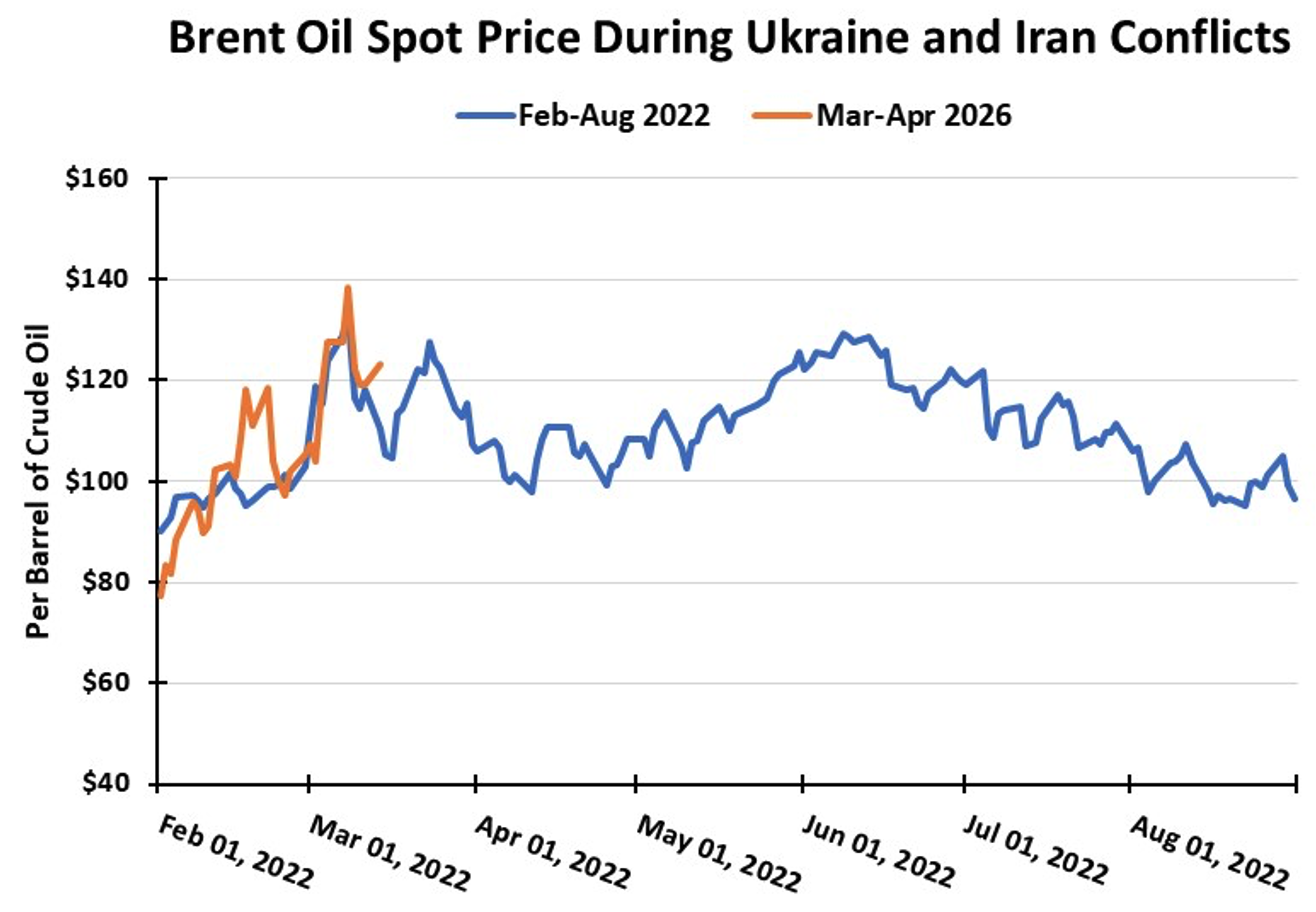

As the war continues, we wonder if oil prices will follow the path they did in 2022 following Russia’s invasion of Ukraine. An outcome of extended high oil prices will be increased industry exploration, as the world needs more reserves, and especially greater production outside of the Hormuz chokepoint.

Natural Gas

The role of domestic natural gas in the global energy industry is growing. While the world’s gas market is dealing with the Hormuz closure that shut in 20 percent of global supply, the question of the long-term impact of Iran’s attacks on Qatar’s LNG facilities remains. Qatar has announced that the damage to its liquefaction plant will require five years to repair. This means it will be forced to declare force majeure on LNG contracts for up to 17% of its capacity. That equates to 12.8 million tons per year, and will cost the national gas company approximately $20 billion in lost revenue annually.

Without Qatar’s LNG supplies, consuming nations are becoming desperate for gas, forcing them to bid aggressively for US and other nations’ output. Ships on their way from the US Gulf Coast to Europe are reversing course and heading toward Asian nations. After being outbid for US LNG shipments, Europe is figuring out how it can access Russian LNG cargoes.

The newest US LNG export terminal, Golden Pass, located on the Sabine Pass, shipped its first cargo on April 22. The terminal is a joint venture of Exxon-Mobil and Qatar-Energy. The two also partner in Qatar’s LNG terminals. This is the first of three processing trains at the plant, with an eventual annual output of 18 million metric tons. Reportedly, the first cargo is heading to Italy to replace LNG that could not be delivered from Qatar’s Persian Gulf facilities.

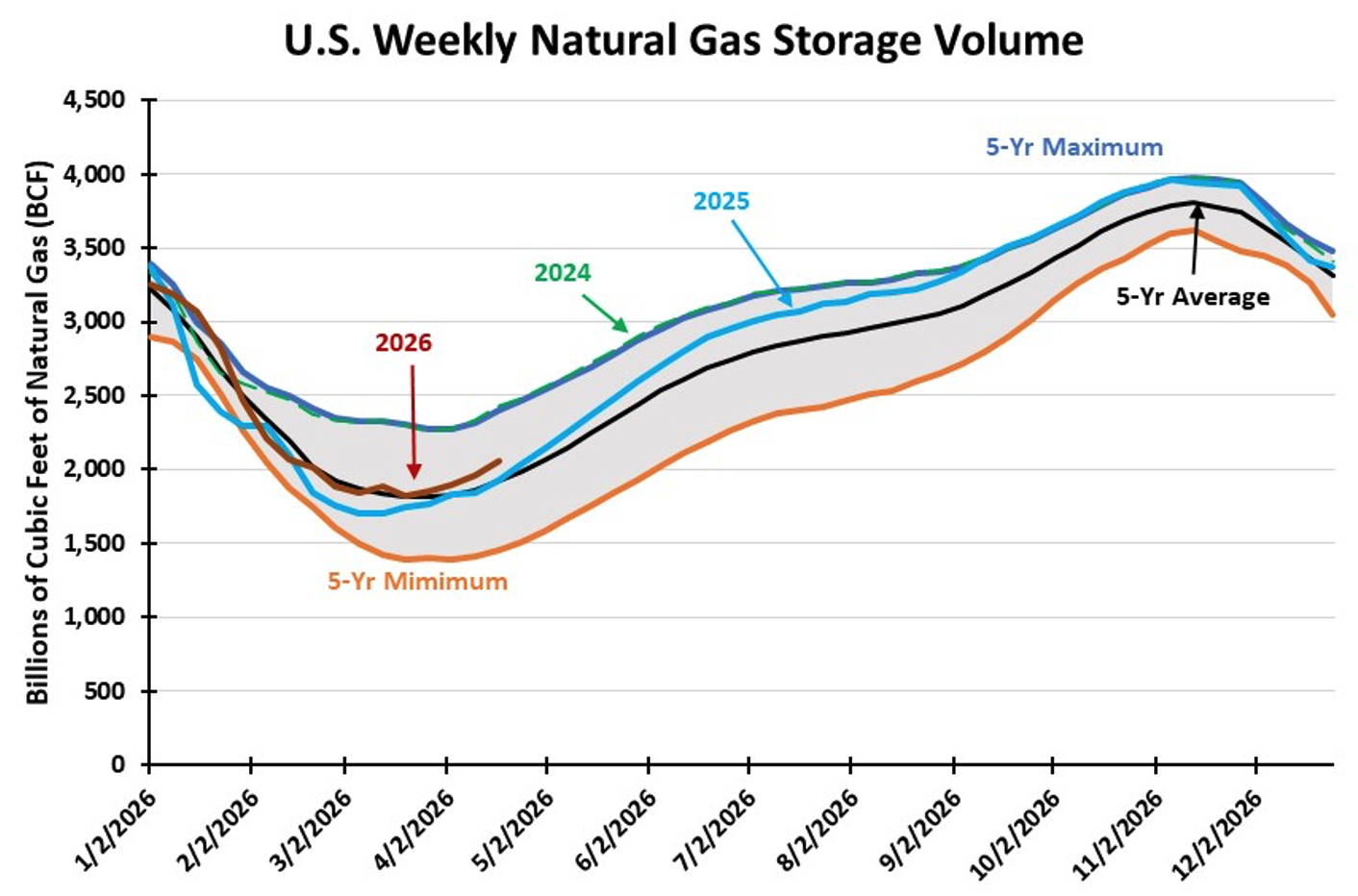

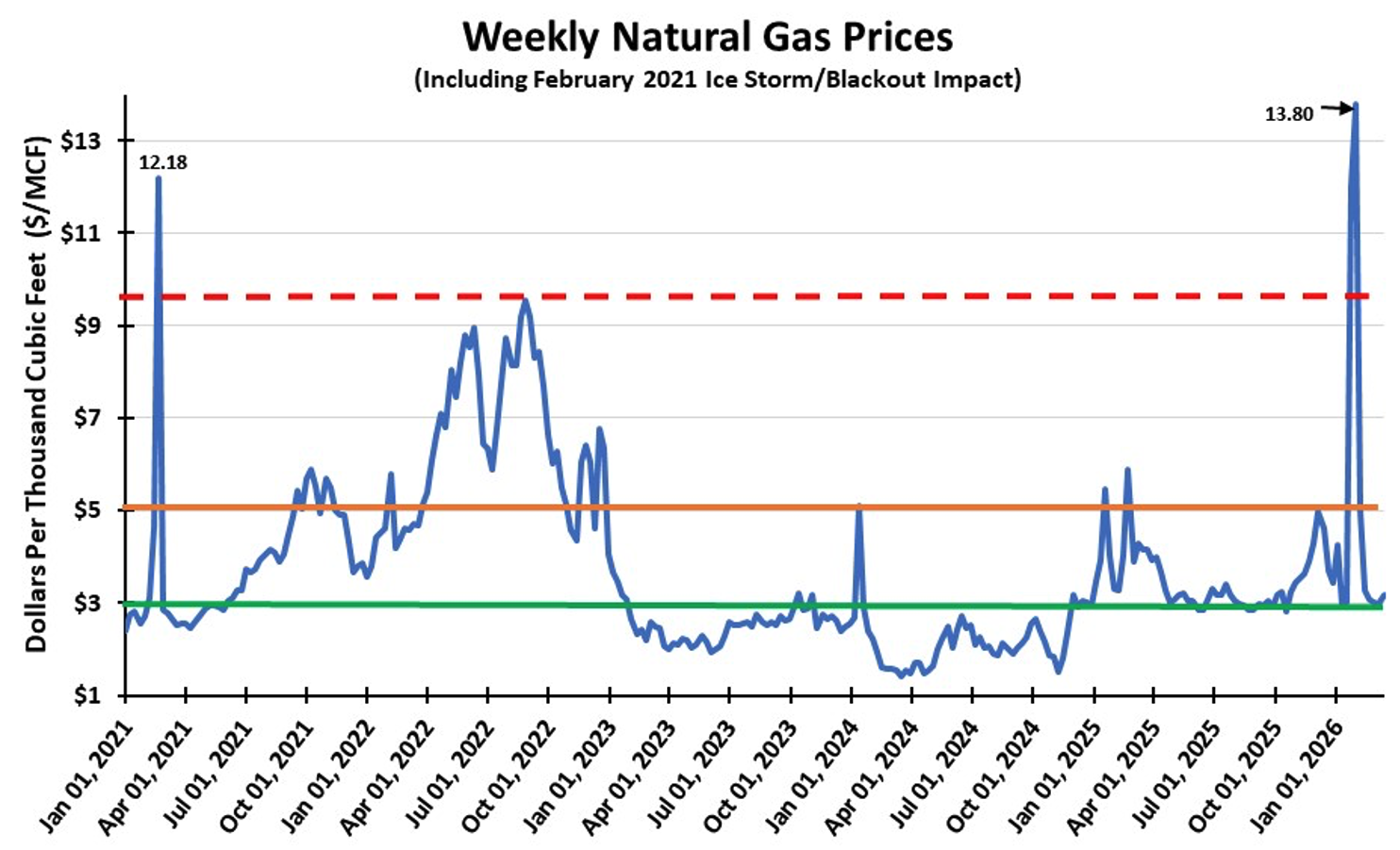

Surprisingly, despite increased bidding for American LNG cargoes, domestic gas prices have fallen below $3 per thousand cubic feet. Additionally, the domestic gas industry has begun rebuilding storage for next winter. The latest storage figures show that volumes are above the 5-year average and the supply in storage at this time last year. Such storage progress is why gas prices remain depressed, as buyers do not have to pay higher prices to attract supply, underscoring our abundant gas resources.

The US gas industry is working to expand pipeline capacity from Texas gas-producing fields to the Gulf Coast to boost LNG export volumes. We are also seeing more pipelines in Texas to deliver gas to generators powering data centers under construction in the state.

The industry has also begun building gas pipelines to move greater volumes from the Appalachian region to the Northeast, where a capacity shortage boosts winter prices. More pipeline capacity will also be needed in the Middle Atlantic region to meet the swelling demand from massive data centers under construction, which natural gas-fired generators will power.

A reality becoming evident is that the US economy is no longer oil-based but has become gas-based. Gas remains a cleaner fuel than crude oil, which makes it the most desirable fuel for dispatchable electricity generation, and the data center boom is driving gas demand.

Is History About to Repeat Itself with Oil Prices Following the 2022 Path?

Domestic Gas Markets Appear Immune to the Fallout from the War in Iran

This feature appeared in ON&T Magazine’s 2026 May Edition, Subsea Robotics, to read more access the magazine here.