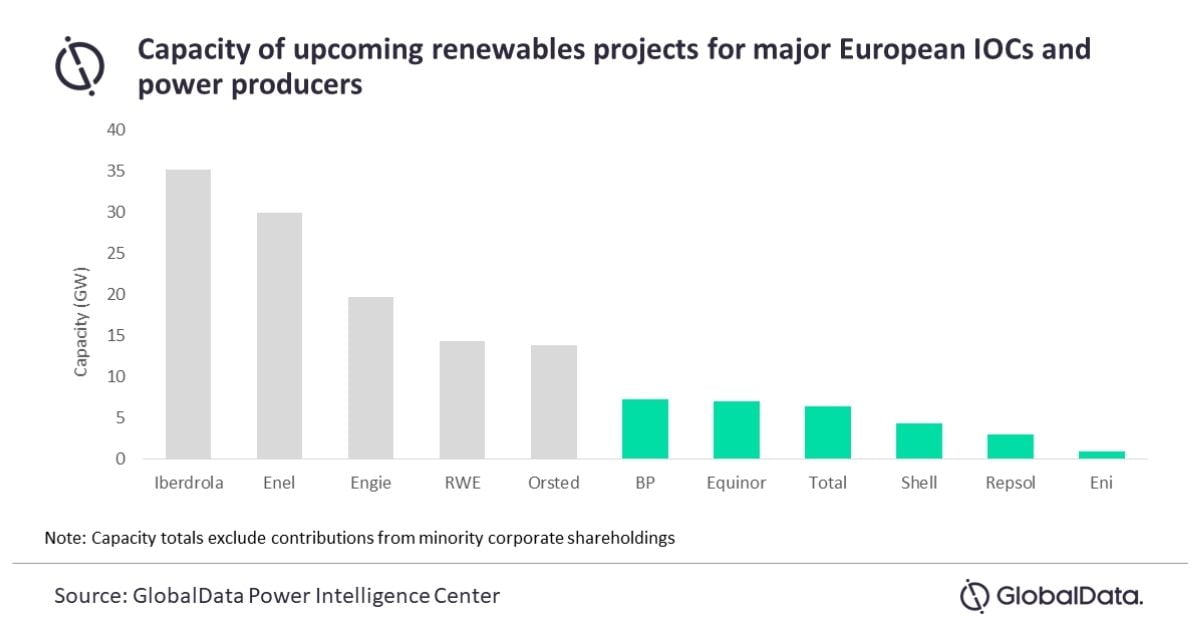

The top six European firms have over 28GW of renewables capacity in the pipeline, with BP, Total and Equinor making up over 70% of this. However, the scale of these companies’ developments still lags behind major power sector incumbents, says GlobalData, a leading data and analytics company.

Will Scargill, Managing Oil and Gas Analyst at GlobalData, commented: ‘‘IOCs’ current development portfolios are still significantly smaller in scale than those of incumbents in the power sector. However, long-term targets suggest an ambition to make up this ground – with BP’s 2030 target of 50GW significantly exceeding Orsted’s target of 30GW.

“The rapid build-out of European IOCs’ renewable portfolios is encouraging as they look to position themselves for the energy transition. However, lofty ambitions do come with significant risk – particularly as they will still look to their oil and gas businesses to be the major cash generators through the medium term. A weak oil and gas market could leave companies unable to fully fund their renewables growth plans, leaving them with a diminished position in the overall energy market.’’

Oil and gas companies looking to transition into the renewables are making significant moves in the mergers and acquisitions (M&A) space to support their growth ambitions. Recent months have seen Total announce a flurry of deals in the wind and solar sectors, while BP announced its entry into offshore wind with a $1.1bn deal to partner with Equinor in US developments.

Scargill continued: ‘‘Solar PV and offshore wind developments account for most of IOCs’ renewables development pipelines. Solar has the benefit of low costs and a short investment cycle, supporting rapid capacity build-out, while offshore wind is expected to see the fastest growth within renewables over the next decade and has the benefit of exploiting oil companies’ experience in offshore development.’’