Westwood has reviewed each of the licenses offered to identify the potential storage targets in depleted hydrocarbon reservoirs and saline aquifers. In addition, an assessment of successful applicants and potential bidders have been provided, based on company announcements, ownership of existing carbon storage licenses as well as proximity of hydrocarbon licenses and infrastructure. A summary of the Round is provided below, and the full analysis of potential storage targets and bidders is available on request.

The Round opened on June 14, 2022, and by the application deadline of September 13, 2022, a total of 26 bids were received from 19 companies for the 13 areas available. Offers have been made in all 13 areas, with some areas split into multiple licenses. The total acreage offered was c. 12,230 km2 from a total of c. 15,702 km2 that was offered in the Round. The SNS area had eight areas available to bidders and was the most hotly contested region with 13 provisional license awards made by the NSTA. The Work Program for each potential license has not been released but at the EGC1 conference in Aberdeen on May 18, 2023, the NSTA stated that five firm wells or tests, nine contingent wells or tests, plus four firm and five contingent new seismic acquisition work programs have been committed to, if all offered licenses are accepted.

While the NSTA requested that companies do not announce their awards, Spirit Energy has confirmed it has been offered EIS Area 1, which supports the company’s ambition to establish its Morecambe Net Zero Cluster. EnQuest has confirmed it has been offered four licenses in NNS Area 1 and NNS Area 2. Neptune Energy is understood to have been awarded three licenses and Perenco, with partner Carbon Catalyst, confirmed it has been offered licenses in the SNS. Synergia Energy announced that one of the two applications it made was under consideration by the NSTA. Westwood assumes this to have been successful and is negotiating terms with the NSTA. It is also understood that BP, Equinor and Eni have been successful as well as one or more of the participants in the Acorn CCS project, Storegga, Shell, Harbour Energy and NSMP. Acceptance of the awards is expected in the coming weeks and if any company declines an offer, due to the proposed work program or area offered being smaller than applied for, the NSTA will offer the license to another company that had applied for the same area.

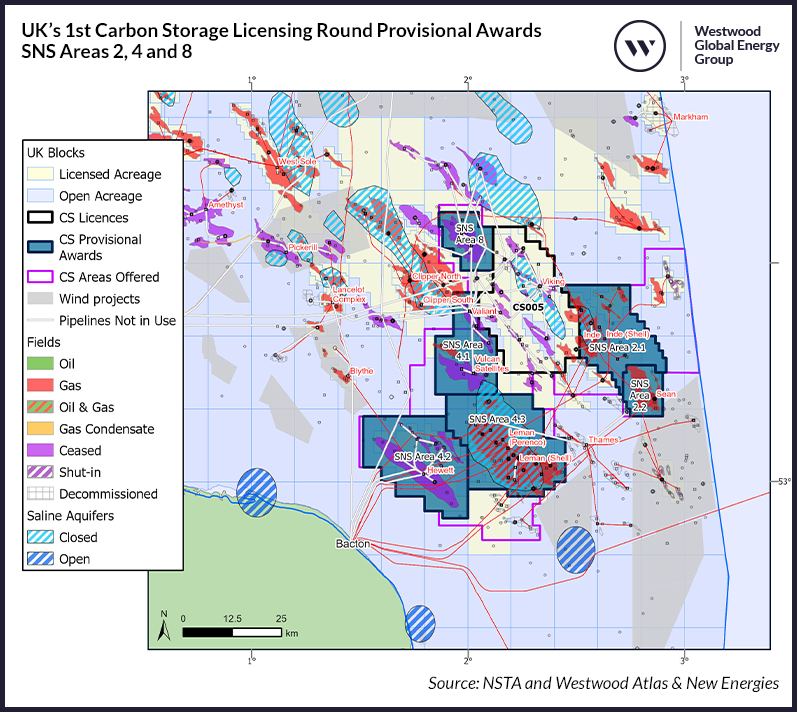

Figure 2: UK’s 1st Carbon Storage Licensing Round Provisional Awards SNS Areas 2, 4 And 8. Source: NSTA, Westwood Atlas and New Energies

Figure 2: UK’s 1st Carbon Storage Licensing Round Provisional Awards SNS Areas 2, 4 And 8. Source: NSTA, Westwood Atlas and New Energies

The new sites offer significant storage opportunity, storing up to 10% of the UK’s annual emissions. The UK has provisionally awarded 20 carbon storage licenses, a threefold increase in active licenses in the country. Alongside legally binding net zero targets, and in the wake of significant financial investment being allocated to support CCS, it marks a major step in the development of the industry.

Interest in the Round was high and there will be companies that are disappointed with the results. Westwood’s analysis has identified many companies that are likely to have applied for acreage based on ownership of existing oil and gas infrastructure and CS licenses, however, they may not all have been successful. It is not yet clear how the CS licenses will impact the existing E&P operators still producing within the awarded acreage.

Within the full report, data and spatial analysis is derived from Westwood’s integrated Atlas and Atlas New Energies products, leveraging our knowledge and experience of the UKCS, to answer questions such as:

- What are the potential storage targets?

- Who are the potential bidders and successful applicants?

- Why was acreage that was made available in the Round not offered within the awarded licenses?

- How might co-location with oil and gas licenses, existing carbon storage licenses, offshore windfarms, and decommissioning license holders have impacted the awards?

As an example, Figure 2 shows the license offers and the potential storage targets in SNS Areas 2, 4 and 8.

By:

Emma Cruickshank, Head of Northwest Europe Research

[email protected]

Stuart Leitch, New Energies Research Manager

[email protected]

Catherine Horseman-Wilson, Senior Analyst – Northwest Europe

[email protected]

Alyson Harding, Technical Manager – Northwest Europe

[email protected]