Identifying an urgent need for a risk-based assessment of the offshore wind pipeline, Westwood developed its new Project Certainty feature for WindLogix. It draws actionable insights based on the risk profile of each developer’s pipeline, enabling a more targeted approach for investment allocation.

In its Project Certainty White Paper, the analysis goes on to reveal that developers such as TotalEnergies and BP have the highest risk profiles, with substantial pipelines but limited or no operational capacity, compared to Orsted and RWE with sizeable track records and a less ‘risked’ unsanctioned portfolio.

(Image credit: Westwood WindLogix)

(Image credit: Westwood WindLogix)

Bahzad Ayoub, Senior Analyst – Offshore Wind, Westwood said: “Offshore wind market uncertainty is rife. Growing diversity of developers in the marketplace, combined with evolving development and commercialization approaches has created a complex landscape. This is compounded further by the diversification of the investor landscape, with oil and gas majors, public investment funds, and even fashion houses entering the sector. However, despite this uncertainty, there is significant opportunity ahead to be capitalized on, but we must first understand the risk.”

Bahzad continues: “When viewed collectively, our current projections reveal a pipeline that faces sizeable risks before reaching FID, with only 9% of capacity ‘Probable’ with the remaining 51% ‘Possible’ and 40% ‘Risked’.”

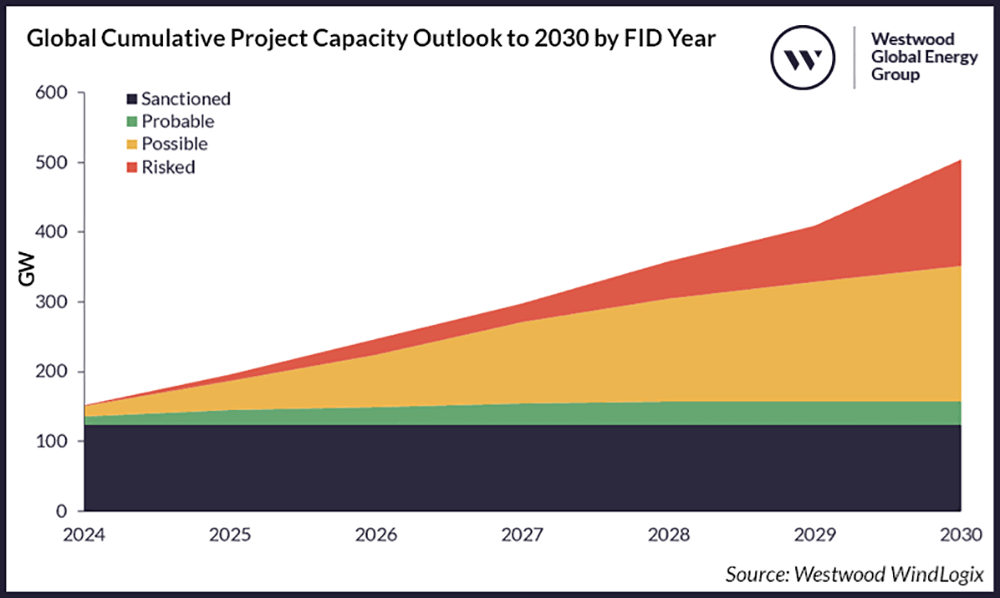

![]() Westwood has formulated three scenarios leveraging project certainty statuses to estimate the potential offshore wind capacity that could reach FID by 2030. These scenarios offer deeper insight into the market’s future, revealing the potential pace of project investments and knock-on effect it has on supply chain opportunities. One potential High scenario reaches 504GW of cumulative sanctioned capacity by 2030, with the Medium and Low cases reaching only just over 351GW and 157GW respectively.

Westwood has formulated three scenarios leveraging project certainty statuses to estimate the potential offshore wind capacity that could reach FID by 2030. These scenarios offer deeper insight into the market’s future, revealing the potential pace of project investments and knock-on effect it has on supply chain opportunities. One potential High scenario reaches 504GW of cumulative sanctioned capacity by 2030, with the Medium and Low cases reaching only just over 351GW and 157GW respectively.

Europe dominates across all three scenarios, forecast to account for the highest amount of cumulative capacity (208GW) that will reach FID by 2030, of which a large proportion (47%) sit within the ‘Possible’ certainty status. The Rest of Asia (RoA) reflects the greatest extent of ‘Risked’ capacity within the share of the region’s pipeline, with the Rest of the World (RotW) next in line, in large part due to immature and evolving offshore wind markets and limited developer track record.

Offshore wind projects in the US account for 67% of the region’s total pipeline capacity. Despite the delays and cancellations that the US has been facing – due to the mismatch between rising costs and expected revenues – the number of ‘Risked’ projects remains relatively small.

The Project Certainty White Paper is available for download and the feature is available to all WindLogix subscribers today.